1. Introduction

Are you self-employed in the UK, navigating the world of invoicing, client work, and the freedom of being your own boss? While the perks are undeniable, one aspect that often causes a headache is the annual Self Assessment tax return, which is a crucial part of running your business. Unlike employees who have tax automatically deducted, sole traders, freelancers, delivery/minicab/uber drivers and small business owners must report their own earnings and pay the correct tax and National Insurance contributions (NICs). But fear not!

This comprehensive guide, we’ll walk you through what Self Assessment is, who needs to file, the key deadlines, and how to calculate what you owe. Whether you’re just starting out or preparing for another tax year, this guide will help you stay compliant and avoid costly penalties.

2. Understanding Self Assessment

In the UK, if you're self-employed and earn over £1,000 in a tax year (which runs from 6 April to 5 April the following year), you're required to register for Self Assessment with HMRC. Unlike employed individuals whose tax is typically deducted at source (PAYE), you're responsible for calculating and paying your own Income Tax and National Insurance Contributions (NICs). While it might seem daunting at first, breaking it down into manageable steps makes it much less stressful.

So, you must file a Self Assessment tax return if:

-

You earn more than £1,000 from self-employment in a tax year (6 April to 5 April).

-

You receive untaxed income, such as rental income, dividends, or overseas earnings.

-

You’re a company director or run a limited company and receive income outside PAYE.

3. Key Aspects of Your Self Assessment Tax Return

a. Registering for Self Assessment

This is your crucial first step! You must register with HMRC by 5 October following the end of the tax year in which you started self-employment. For example, if you started in June 2025, you'd need to register by 5 October 2026. Registering late can lead to penalties, so it's always best to do it as soon as possible. Once registered, HMRC will send you a Unique Taxpayer Reference (UTR) number, which you'll need for all your tax affairs. You'll also be able to set up a Government Gateway account for online filing.

b. Understanding Your Taxable Income

Your taxable income as self-employed is your total business income minus your "allowable business expenses." This means:

Taxable Income = Total Income – Allowable Expenses

This is your profit, and it's what you'll pay tax on. Keeping meticulous records of all your income and expenses throughout the year is paramount.

Allowable Business Expenses:

These are costs incurred wholly and exclusively for your business. Examples include:

-

Office Costs: Stationery, postage, office rent, or a portion of your utility bills if working from home.

-

Travel Expenses: Business-related mileage, public transport fares, and accommodation.

-

Marketing Costs: Advertising, website hosting, and promotional materials.

-

Professional Fees: Accountant's fees, legal advice directly related to your business.

Trading Allowance vs. Expenses:

If your total business expenses are less than £1,000, you might consider claiming the £1,000 trading allowance instead of itemising individual expenses. However, if your expenses exceed £1,000, it's generally more beneficial to deduct your actual expenses.

c. Personal Allowance

Most individuals in the UK receive a tax-free Personal Allowance. For the 2025/26 tax year, the standard Personal Allowance is £12,570. This means you don't pay Income Tax on the first £12,570 of your taxable income. Be aware that your Personal Allowance reduces if your income exceeds £100,000 and is completely withdrawn if you earn over £125,140.

d. Self-Employment Income Tax Rates

The Income Tax rates for self-employed individuals are the same as for employed individuals. Here are the rates for England, Wales, and Northern Ireland (Scottish rates may differ):

| Trading Profits | Tax Rate | Tax Band |

| £0 to £12,570 | 0% | Personal Allowance |

| £12,571 to £50,270 | 20% | Basic Rate |

| £50,271 to £125,140 | 40% | Higher Rate |

| Over £125,140 | 45% | Additional Rate |

e. National Insurance Contributions (NICs)

As a self-employed individual, you'll typically encounter two types of National Insurance Contributions (NICs) which contribute towards certain state benefits, including the State Pension and Jobseeker's Allowance.

For the 2025/26 tax year (which you'll use in your online tax return due by 31 January 2027):

Class 2 NICs:

-

If your annual trading profits are £6,845 or more: You will be treated as having paid Class 2 NICs and will get access to contributory benefits, including the State Pension, through a National Insurance credit, without needing to pay Class 2 NICs.

-

If your annual trading profits are less than £6,845: You do not have to pay Class 2 NICs, but you can choose to pay them voluntarily to protect your National Insurance record and access certain benefits. The voluntary rate for Class 2 NICs for 2025/26 is £3.50 per week.

Class 4 NICs:

These are calculated based on your annual trading profits:

-

0% on profits from £0 to £12,570 (your Personal Allowance band).

-

6% on profits between £12,571 and £50,270.

-

2% on profits over £50,270.

Example Calculation (for 2025/26 profits):

Let's say your annual trading profits are £60,000. You would pay:

Class 2 NICs: You would not pay Class 2 NICs, but you would be credited for them as your profits are above the £6,845 threshold.

Class 4 NICs:

-

Nothing on the first £12,570.

-

6% on the next £37,700 (£50,270 - £12,570) = £2,262.00

-

2% on the final £9,730 (£60,000 - £50,270) = £194.60

-

Total Class 4 NICs = £2,456.60

f. Estimating Your Tax Bill

HMRC provides online tools, such as the "Self-employed ready reckoner," which can help you estimate your tax and National Insurance liabilities. This can be very useful for budgeting and setting aside money throughout the year to cover your tax bill.

g. Submitting Your Self Assessment Tax Return

You can submit your Self Assessment tax return online through the HMRC website. The deadline for online submissions is 31 January following the end of the tax year. For example, for the tax year 2025/26 (ending 5 April 2026), the online deadline is 31 January 2027. Paper returns have an earlier deadline of 31 October. There's also a second payment on account due by 31 July if any balancing payment due.

Key Self Assessment Deadlines

| Task | Deadline |

| Register for Self Assessment | 5 October 2026 |

| Online tax return submission | 31 January 2027 |

| First payment on account | 31 January 2027 |

| Second payment on account | 31 July 2027 |

Late filing or payment can result in penalties and interest charges, so don’t leave it until the last minute.

h. Paying Your Tax Bill

Your tax bill, including Income Tax and NICs, is also due by 31 January following the end of the tax year. You might also need to make "payments on account," which are advance payments towards your next year's tax bill, due on 31 January and 31 July.

i. Corporation Tax for Limited Companies

If you operate your business as a limited company or a limited liability partnership (LLP), you'll also be liable for Corporation Tax on your company's profits, in addition to your personal Self Assessment.

4. Checklist to Submit a Self Assessment Return

-

Register with HMRC if it’s your first time.

-

Track your income and expenses throughout the year.

-

Submit your return online via HMRC's website.

-

Pay any tax and NICs owed by the deadlines.

You can also use HMRC’s Self-employed ready reckoner to estimate your tax bill in advance. GOV.UK also has a portal for guidance, videos, and webinars for Self Assessment for user convenience.

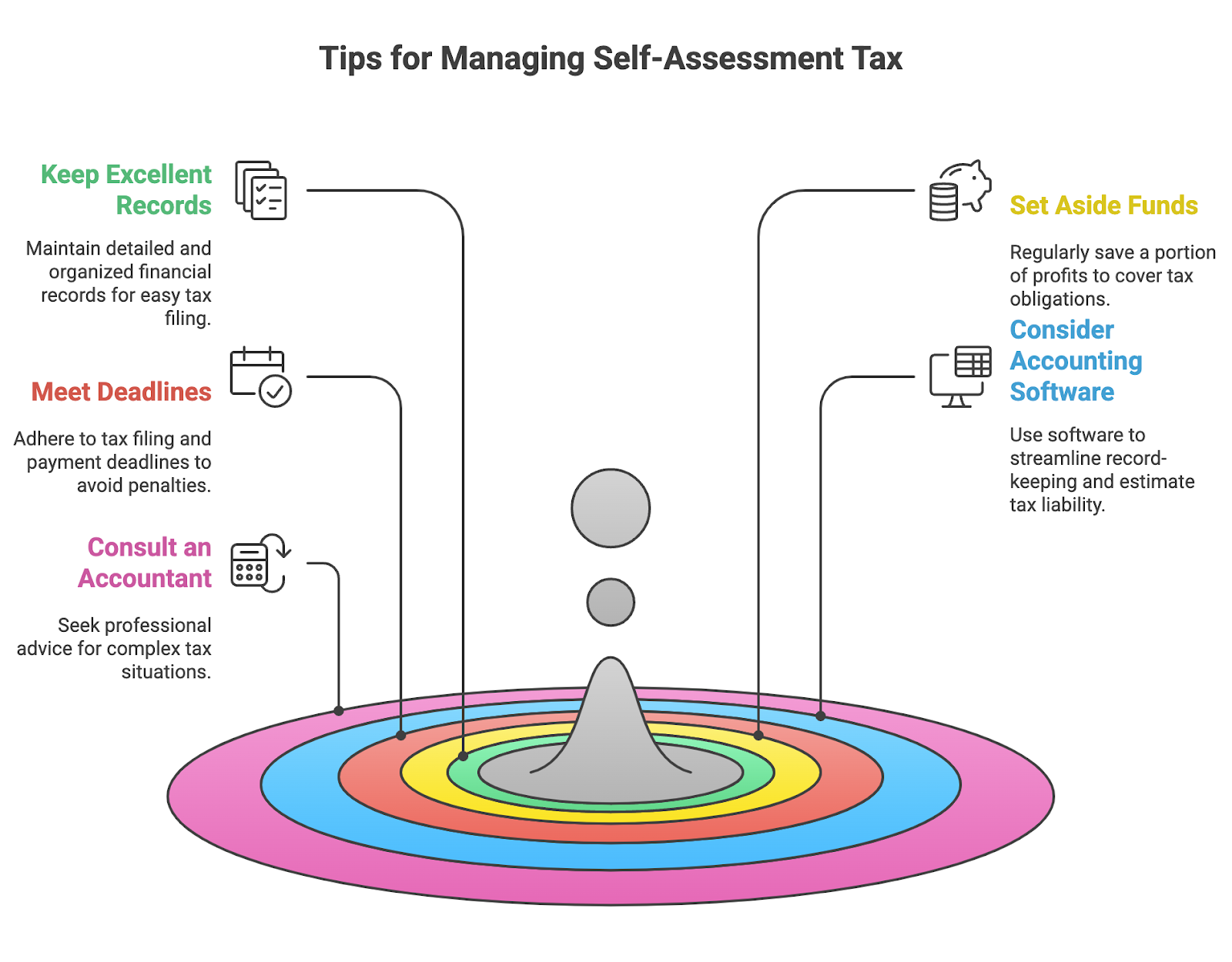

5. Practical Tips for Managing Your Tax Obligations

-

Keep Excellent Records: Maintain detailed, organised records of all your income and expenses. This will make filling out your tax return much easier and help you claim all eligible deductions.

-

Set Aside Funds: A common pitfall for the self-employed is not saving enough for tax. A good rule of thumb is to put aside around 25-30% of your profits regularly to cover your tax and NICs.

-

Meet Deadlines: HMRC penalties for late filing and late payment can be substantial. Mark the key deadlines in your calendar.

-

Consider Accounting Software: Using accounting software can significantly streamline your record-keeping, track expenses, and even help estimate your tax liability in real-time.

-

Seek Professional Advice: If your tax situation is complex, or if you're new to self-employment, don't hesitate to consult a qualified accountant. They can ensure accuracy, maximise your tax savings, and offer invaluable peace of mind.

6. How Can WPC Accountant Help?

Navigating the complexities of Self Assessment can be time-consuming and stressful, taking valuable time away from running your business. At WPC Accountant, we specialise in providing stress-free Self Assessment services, ensuring your compliance and maximising your tax efficiency.

Our expert team can:

-

Help you register for Self Assessment

-

Ensure you claim all allowable expenses

-

Accurately calculate your tax and NICs

-

File your returns on time and avoid penalties

📞 Call us: +44 7380 992174

📧 Email: support@wpcaccountantsltd.co.uk

📅 Book a free consultation: calendly.com/lutfur-workpermitcloud

Let WPC Accountant handle your Self Assessment, so you can focus on what you do best – growing your business.

7. Conclusion

Self Assessment is an integral part of being self-employed in the UK. By understanding the key steps, maintaining good records, and being aware of deadlines, you can manage your tax obligations effectively. Remember, professional assistance from WPC Accountant is always available to simplify the process, save you time, and ensure you remain compliant with HMRC, giving you complete peace of mind.

8. Glossary

| Term | Definition |

| Self Assessment | The system used by HMRC for individuals to report their income and pay Income Tax and National Insurance if it's not automatically deducted (e.g., for self-employed individuals, those with rental income, or high earners). |

| HMRC | Her Majesty's Revenue and Customs, the UK's tax, payments, and customs authority. |

| Tax Year | The period over which income and tax are calculated in the UK, running from 6 April to 5 April of the following year. |

| Unique Taxpayer Reference (UTR) | A 10-digit number issued by HMRC to identify individuals and businesses for tax purposes. You'll receive this after registering for Self Assessment. |

| Allowable Business Expenses | Costs incurred "wholly and exclusively" for your business, which can be deducted from your total income to reduce your taxable profit. |

| Trading Allowance | A £1,000 tax-free allowance for self-employed income or property income. If your gross income from these sources is less than £1,000, you don't need to declare it. If it's over, you can claim this allowance instead of itemising expenses (if more beneficial). |

| Personal Allowance | The amount of income you can earn in a tax year before you start paying Income Tax. For most people, this is £12,570 for the 2025/26 tax year. |

| Income Tax | A tax on your earnings, including profits from self-employment, salaries, rental income, and savings interest. |

| National Insurance Contributions (NICs) | Payments made by working individuals to qualify for certain state benefits, such as the State Pension and Jobseeker's Allowance. Self-employed individuals typically pay Class 2 and Class 4 NICs. |

| Payments on Account | Advance payments towards your next year's Self Assessment tax bill, usually made in two instalments on 31 January and 31 July. This applies if your previous year's tax bill was over £1,000 and wasn't largely collected at source. |

| Trading Profits | Your self-employed income after deducting allowable business expenses. |

| Allowable Expenses | Business-related costs that can be deducted from income before calculating tax. |

| Class 2 NICs | A flat-rate contribution paid weekly by self-employed individuals with profits over the lower threshold. |

| Class 4 NICs | A percentage-based contribution paid on annual profits above certain thresholds. |

| Corporation Tax | A tax on the profits of limited companies and some organisations. |

Frequently Asked Questions (FAQs)

Do I need to file a Self Assessment tax return?

You will generally need to file a Self Assessment tax return if you are self-employed as a sole trader, freelancer, delivery/minicab/uber driver, small business owner and earned more than £1,000 before expenses in a tax year. Other reasons include being a company director (unless for a non-profit and you received no pay or benefits), earning over £100,000, having significant untaxed income from savings, investments, property rental, or foreign sources, or if you need to pay Capital Gains Tax.

When do I need to register for Self Assessment?

If you need to complete a Self Assessment tax return for the first time, you must notify HMRC by 5 October following the end of the tax year in which you started earning the income that requires a return. For example, if you became self-employed in June 2025, you must register by 5 October 2026.

What are the key deadlines for Self Assessment?

The main deadlines are: 5 October after the tax year ends to register if you're new to Self Assessment; 31 January after the tax year ends for online submission of your tax return; and 31 January after the tax year ends to pay any tax due for the previous tax year, along with your first payment on account. There's also a second payment on account due by 31 July.

What happens if I miss a Self Assessment deadline?

Missing deadlines can lead to penalties and interest charges from HMRC. A late filing penalty of £100 is automatically applied even if you owe no tax. Further penalties can accumulate the longer the return is outstanding, and interest is charged on unpaid tax from the due date.

What records do I need to keep for my Self Assessment?

You must keep accurate and detailed records of all your business income and expenses. This includes bank statements, receipts for purchases, sales invoices, and any other relevant financial documents. HMRC requires you to keep these records for at least five years after the 31 January submission deadline for the relevant tax year.

Can I pay my Self Assessment tax bill in instalments?

While the main payment deadlines are 31 January and 31 July (for payments on account), you can set up a Budget Payment Plan with HMRC to spread the cost of your tax bill through regular payments throughout the year. This can help you manage your cash flow.

Do I need an accountant to do my Self Assessment?

You are not legally required to use an accountant for your Self Assessment. However, many self-employed individuals choose to do so to ensure accuracy, compliance, maximise allowable expenses, and save time. An accountant can also offer expert advice on tax planning specific to your business.

Do I need to file a Self Assessment tax return if I only earn a small amount?

Yes, if your self-employment income exceeds £1,000 in a tax year, you must file a Self Assessment return. If it’s under that threshold, you may be eligible for the trading allowance, but registering may still be beneficial if you want to claim expenses.

What National Insurance contributions do I pay as a sole trader?

Self-employed individuals pay Class 2 and Class 4 NICs. Class 2 is a flat weekly amount, while Class 4 is based on your annual profits.

Can I file my tax return online?

Yes, HMRC allows individuals to submit their Self Assessment tax return online through its official website. You’ll need to set up a Government Gateway account if it’s your first time.

Do I need to file a Self Assessment return if I have a limited company?

If you draw income outside PAYE, such as dividends or director's loans, you’ll likely need to file a personal Self Assessment return in addition to your company’s Corporation Tax return.