1. Introduction

Hiring your first employee is an exciting milestone for any business. It signifies growth and a new chapter. However, it also brings new responsibilities, with setting up payroll being one of the most critical. Getting it right from day one is essential for keeping your team happy, your business compliant, and your focus where it should be—on growth.

So, what exactly is payroll?

In the UK, it’s much more than simply transferring wages. It's a comprehensive system for calculating pay, deducting the correct amounts for tax (PAYE), National Insurance, and other contributions, and reporting this information to His Majesty's Revenue and Customs (HMRC) in real-time.

This guide will walk you through everything you need to know, from the initial setup decisions to your ongoing duties.

2. The First Big Decision: In-House or Outsourced Payroll?

Before you get into the details, you need to decide how you will manage your payroll. There are two primary paths, each with distinct advantages.

Running Payroll In-House

Managing payroll yourself can be a rewarding option, especially for business owners who want complete oversight.

-

The Benefits: You have maximum control over your financial processes and can make last-minute adjustments quickly. It can also be more cost-effective if you have the time and expertise, and it keeps sensitive employee data within your direct control.

-

The Considerations: In-house payroll demands a significant time investment and a deep understanding of complex, ever-changing legislation. The risk of errors and non-compliance, which can lead to hefty fines from HMRC, rests entirely on your shoulders.

Outsourcing Your Payroll

For many growing businesses, outsourcing to a specialist like an accountant or a dedicated payroll bureau is the more strategic choice.

-

The Benefits: You gain instant access to expert knowledge, ensuring you remain compliant with all regulations, from National Minimum Wage to auto-enrolment pensions. It frees up your valuable time, removes administrative headaches, and significantly reduces the risk of costly mistakes.

-

The Considerations: This option comes with a cost, though it is often offset by the time saved and penalties avoided. You will need to partner with a provider who is reliable, accredited, and uses secure, modern systems.

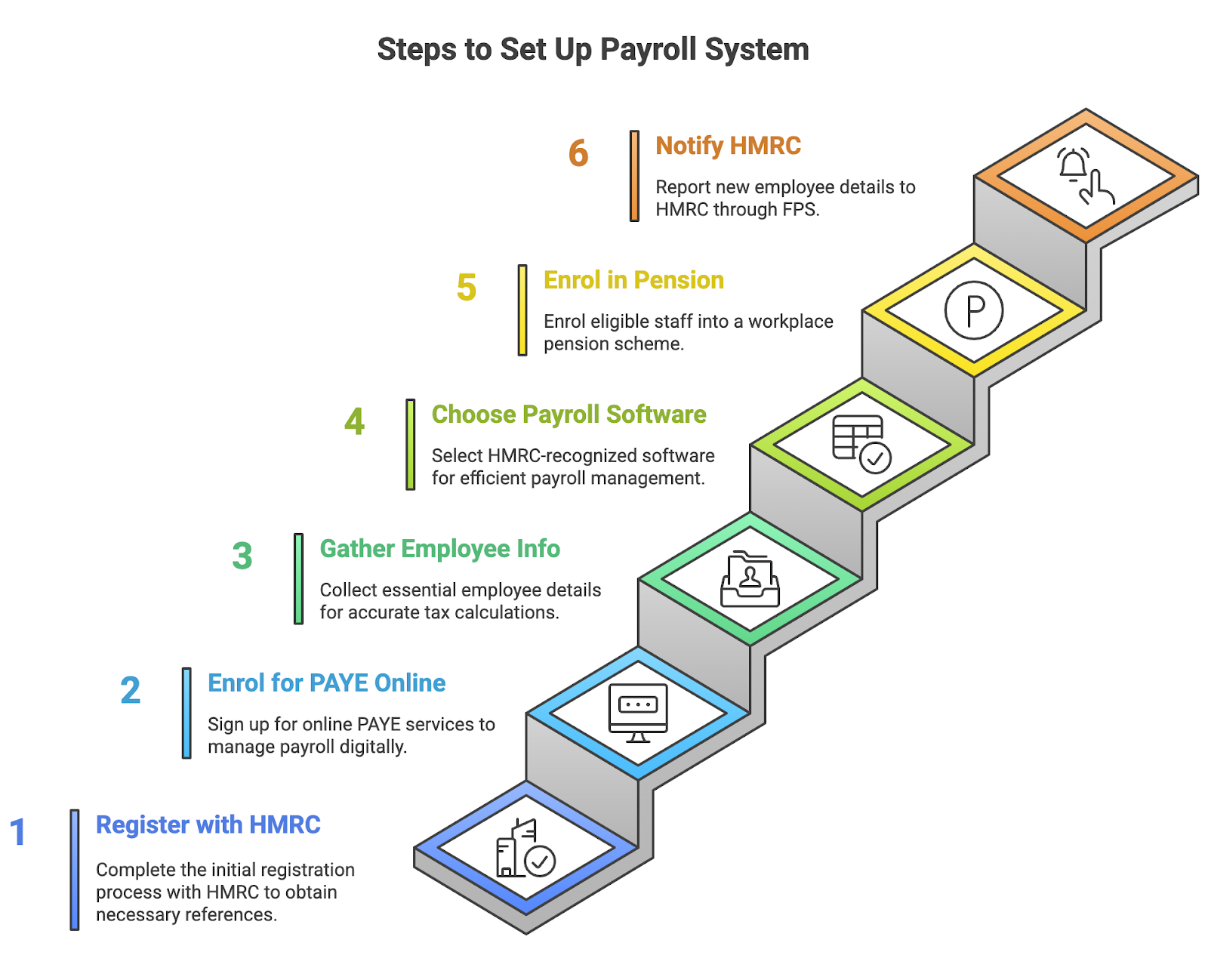

3. The Core Steps to Setting Up Your Payroll System

If you've decided to manage payroll in-house or want to understand the process your provider will follow, here are the essential setup steps.

1. Register as an Employer with HMRC

This is the non-negotiable first step. Before you can pay anyone, you must register as an employer with HMRC. You should do this at least two weeks before your first payday, but you can't register more than two months in advance. Once registered, HMRC will provide you with an employer PAYE reference number, which is essential for all payroll reporting.

2. Enrol for PAYE Online

Most employers are automatically enrolled when registering, but if not, sign up via the HMRC PAYE portal.

3. Gather Essential Employee Information

To add a new employee to your payroll, you need specific information to calculate their tax correctly. You will need their:

-

Full name, address, and date of birth.

-

National Insurance (NI) number.

-

P45 from their previous job. If they don’t have a P45, you must use

-

Details about any

4. Choose Your Payroll Software

An effective payroll system is impossible without the right tools. You must use HMRC-recognised software that can:

-

Calculate pay and deductions accurately.

-

Report payroll information to HMRC in real-time (known as Real Time Information or RTI).

-

Generate legally compliant

-

Work out

5. Enrol Eligible Staff into a Workplace Pension

Under UK law, all employers must provide a workplace pension scheme and automatically enrol eligible employees. This is a crucial compliance step. You are responsible for making deductions from your employees' pay and contributing as an employer.

6. Tell HMRC About Your New Employee

Once you have your new employee’s details set up in your payroll software, you must formally notify HMRC. Under the Real Time Information (RTI) system, you do this by including the new employee's details in your next Full Payment Submission (FPS). This report must be sent to HMRC on or before the employee's first payday, effectively registering them under your PAYE scheme.

4. Your Regular Payroll Duties: A Month-by-Month Look

Once you are set up, payroll becomes a cyclical monthly or weekly task. Here’s what you need to do every time you pay your staff.

-

Calculate Pay and Deductions: For each employee, you'll calculate their gross pay and then deduct income tax (PAYE),

-

Expenses and Benefits: Items like uniforms or company cars must be reported and may affect tax liabilities.

-

Issue Payslips: You are legally required to provide each employee with a

-

Report to HMRC: Each time you run payroll, you must send a

-

Pay HMRC: You must pay the tax and

5. Key Compliance Areas to Master

Getting payroll right means staying on top of key legal requirements.

-

National Minimum Wage: You must pay your staff at least the

-

Statutory Payments: You may need to process statutory pay for employees on leave, such as

-

Record Keeping: HMRC requires you to keep accurate payroll records for at least three years from the end of the tax year they relate to. This includes details of pay, deductions, leave, and tax code notices. Poor record-keeping can result in fines of up to £3,000.

6. How Can WPC Accountants Help?

At WPC Accountants, we understand that managing payroll can be a complex and time-consuming task for business owners. Getting it right is crucial for compliance and keeping your team happy. We take the stress out of payroll, ensuring your staff are paid accurately and on time, every time.

Our dedicated team handles everything from HMRC registration and RTI submissions to pension auto-enrolment and generating payslips. By partnering with us, you can free yourself from the administrative burden and focus on what you do best—running and growing your business.

Let us help you stay compliant, efficient, and in control.

📞 Call us: +44 7380 992174

📧 Email: support@wpcaccountantsltd.co.uk

📅 Book a free consultation: calendly.com/lutfur-workpermitcloud

7. Conclusion

Setting up and running a payroll system is a foundational part of being an employer in the UK. While the responsibilities—from HMRC registration and RTI reporting to accurate record-keeping—can seem daunting, they are entirely manageable. The key is to decide on the right approach for your business, whether that’s a hands-on in-house method or partnering with an expert service.

By understanding your obligations and using the right tools or support, you can build a payroll process that is smooth, compliant, and lets you and your employees thrive.

8. Frequently Asked Questions (FAQs)

Do I need to run payroll if I'm the only employee of my limited company?

Yes, if you are a director taking a salary from your own limited company, you are considered an employee. You must operate a PAYE payroll scheme to report your earnings and pay the correct Income Tax and National Insurance contributions to remain compliant with UK law.

What happens if I miss a payroll deadline or make a mistake?

Missing a deadline for sending a Full Payment Submission (FPS) or paying HMRC can lead to late-filing penalties and interest charges. If you make an error on a payroll run, you can usually correct it on your next FPS. It is crucial to act quickly to fix any mistakes and to inform HMRC if you have a valid reason for a late submission to avoid potential penalties.

How soon do I need to register as an employer before my first payday?

You should aim to register as an employer with HMRC at least two weeks before your first planned payday. This allows enough time for HMRC to process your registration and send you the necessary PAYE reference numbers. HMRC typically takes up to 5 working days to issue your employer PAYE reference number. Please note that you cannot register more than two months before you start paying your staff.

What is the difference between gross pay and net pay on a payslip?

Gross pay is the total amount you earn before any deductions are taken out. Net pay is the final "take-home" amount you receive in your bank account after all deductions, such as Income Tax, National Insurance, pension contributions, and any student loan repayments, have been subtracted from your gross pay.

What happens if I make a mistake in payroll submissions?

Errors in payroll, such as late or incorrect submissions, can lead to HMRC penalties and affect employee benefits like Universal Credit. Using reliable software or expert services helps avoid these issues.

How often should I pay my employees?

Payment frequency depends on your agreement with employees. Most UK employers run payroll monthly, but weekly or biweekly options are also common.

Do I need to issue payslips to employees?

Yes. You are legally required to provide employees with a payslip on or before payday, showing gross pay, deductions, and net pay.

What’s included in payroll deductions?

Typical deductions include Income Tax, National Insurance, student loans, pensions, and other voluntary schemes like payroll giving.

What records should I keep for payroll?

You must keep records of payments, deductions, employee absences, tax code notices, and benefits for at least three years for HMRC compliance.

9. Glossary

| Term | Definition |

|---|---|

| PAYE | Pay As You Earn. This is HMRC's system for collecting Income Tax and National Insurance directly from employment earnings. |

| HMRC | His Majesty's Revenue and Customs. The non-ministerial department of the UK Government responsible for the collection of taxes. |

| RTI | Real Time Information. The system that requires employers to report payroll information to HMRC online every time they pay an employee. |

| FPS | Full Payment Submission. This is the report sent to HMRC under the RTI system, detailing employee payments and deductions for a specific pay period. |

| P45 | A document an employee receives from their previous employer. It details their total pay and the tax paid in that job for the current tax year. |

| P60 | A summary statement given to each employee at the end of the tax year (5th April), showing their total pay and deductions for the entire year. |

| Auto-Enrolment | A legal requirement for UK employers to automatically place eligible staff into a workplace pension scheme and contribute towards it. |

| Gross Pay | The total amount of an employee's earnings before any deductions, such as tax or National Insurance, are made. |

| Net Pay | The final amount an employee receives after all deductions have been taken from their gross pay. This is often called "take-home pay". |

| Statutory Pay | Legally mandated pay such as Sick Pay, Maternity, and Paternity Pay. |

| Payslip | A document provided to employees showing earnings and deductions each payday. |

| Tax Code | Code used by employers to determine how much tax to deduct from employee wages. |

| Student Loan Deduction | Payroll deduction based on employee income and repayment plan. |